[“Power Through a Possible Recession With Growth Stocks” was originally published on May 13, 2022. It has since been updated and republished.]

Lately, the stock market has been getting crushed. It’s clear that we’re in the middle of a bear market. And it seems likely that the U.S. will see a recession within the next 12 months. That’s if it’s not there already.

That may sound scary. But it shouldn’t be.

Recessionary periods and bear markets create once-in-a-decade buying opportunities in the stock market.

In other words, recession risks are rising, and the broader markets are highly volatile. But we’re growing very bullish on a particular group of stocks right now.

Historically, crises have created opportunities. This time is no different. And the opportunities we’re seeing right now are potentially life-changing.

So, don’t freak out. Don’t run for cover…

The best thing to do during bear markets and crashes is to hunker down in stocks that will soar once the downturn passes.

Watch the Yield Curve in Bear Markets

There’s some spooky data out there that implies that a big economic slowdown — or worse — has arrived.

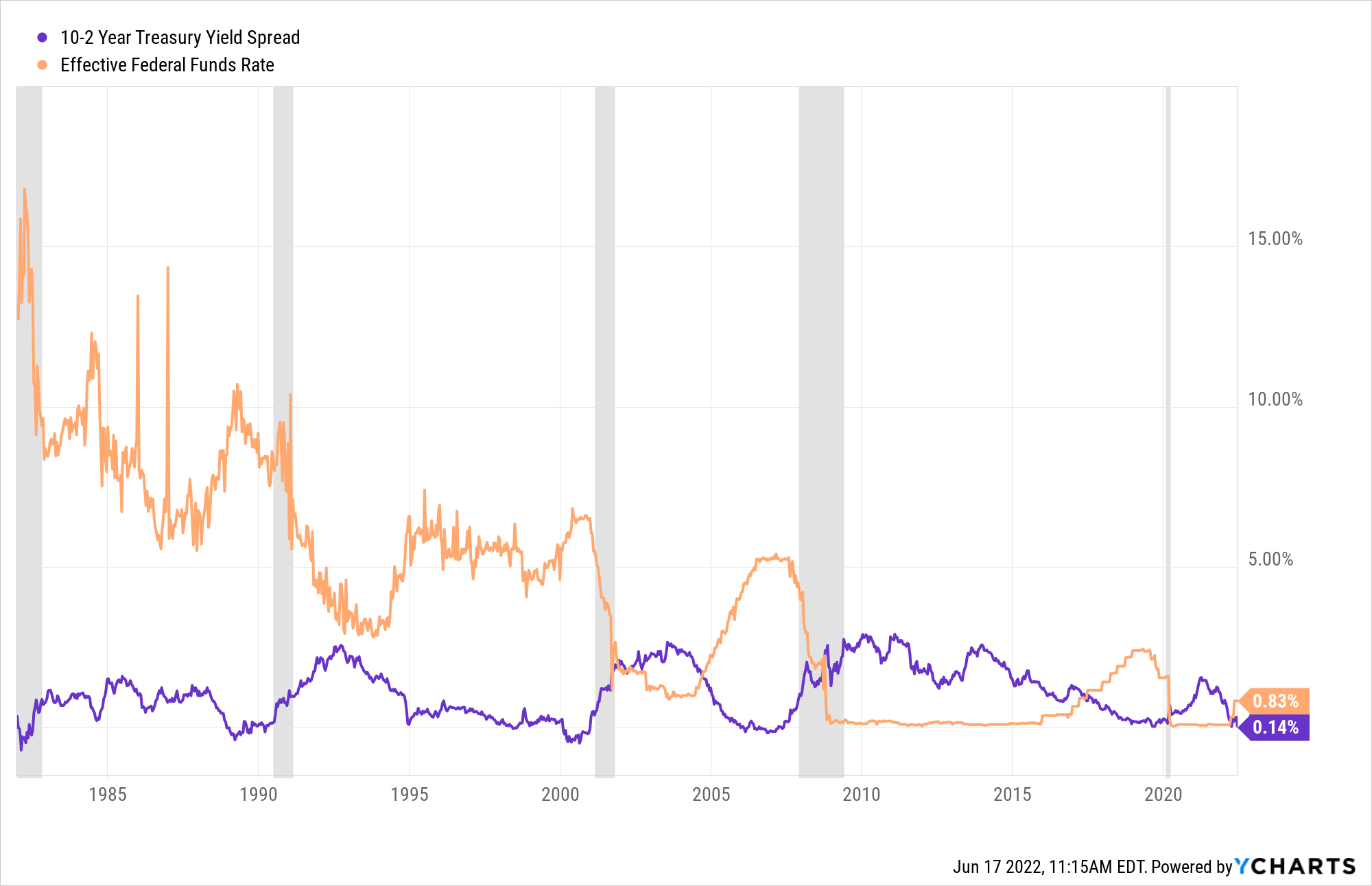

Perhaps the most important of these data points is the spread between the 2- and 10-year Treasury yields. It’s been shrinking rapidly over the past few months. And this past Monday, June 13, the yield curve briefly inverted minus 2 basis points before normalizing.

Recall that a flattening yield curve is the bond market saying that an economic slowdown is coming. And a yield curve inversion has preceded every economic recession since 1980.

Since March, we’ve seen a rapid flattening of the yield curve to below 30 basis points. That’s a bearish dynamic that’s happened only six times since 1982.

Four of those six occurrences were followed by a yield curve inversion within 12 months. And those inversions subsequently spilled into recessions. Two of those six occurrences were not followed by a yield curve inversion (August 1984 and December 1994). Both of those times, an inversion was averted by the Fed cutting rates.

Well, in March, we did see a yield curve inversion. And even still, the central bank has been quite hawkish.

To get a handle on runaway inflation, the Federal Reserve is hiking rates. And such an unprecedented action is expected to happen alongside a war in Europe and a slowing labor market. That’s not a bullish setup.

The Fed had its June meeting on Wednesday of this week. The central bank hiked rates by 75 basis points and signaled for another potential 75-bps hike in July. This is a Fed that will hike more now to hike less later. And it expects the next few big lifts to successfully stomp out inflation.

In other words, we finally have visibility to inflation falling to normal levels. But it will take a lot of rate hikes and some significant economic cooling to get there. And to be frank, a recession is now likely the base case.

Sounds scary but it’s not.

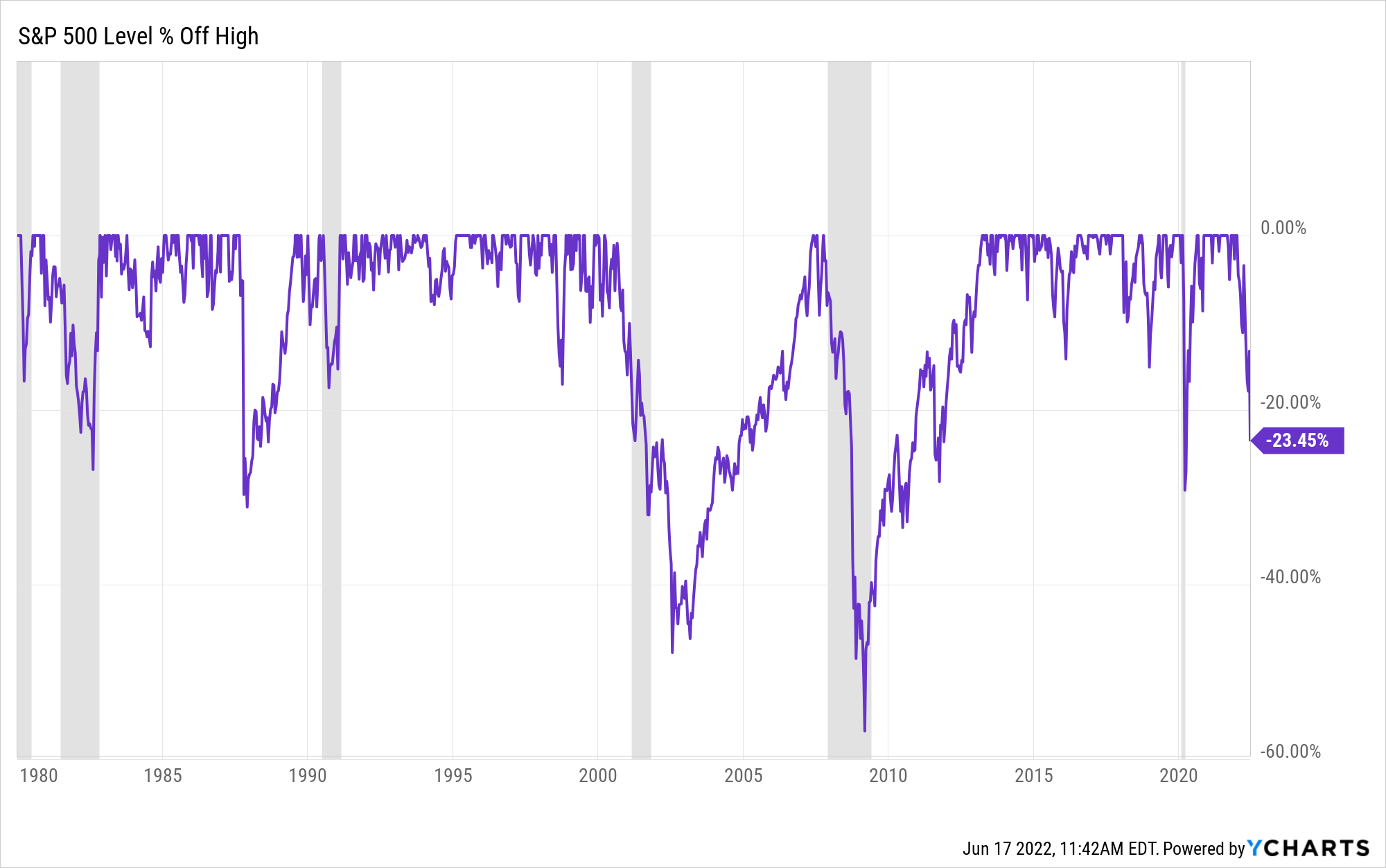

How Much Farther Will Stocks Fall?

In the early 1980s, a U.S. economic recession led to just a 15% drawdown in stocks. The early 1990s recession similarly led to just an 18% drawdown.

Sure, the early 2000s recessions resulted in a 40% stock market collapse, while the 2008 recession sunk stocks by 50%.

But this is not that.

In 2000, we suffered from gross overvaluation. The S&P 500 was trading at 26X forward earnings, with a 10-Year Treasury yield above 5%. Today the market is trading at 22X forward earnings, with a 10-Year yield below 3.4%. Today’s valuation is lower both in absolute and relative terms compared to what we saw in 2000.

Meanwhile, in 2008, the entire U.S. financial system was on the verge of collapse. We don’t have that today. Balance sheets across banks, corporations, and households are cash-heavy and very strong. Interest rates are still relatively low. We do not have another 2008 on the horizon.

So, in the grand scheme of things, we face what will likely be a shallow recession. It’s likely to follow those of the early 1980s and early 1990s, when stocks dropped around 20- to 30%.

Buying the Dip During a Bear Market

Over the past few months, we’ve seen some sharp drops in stocks. And in such an unpredictable climate, it’s far too early to call a bottom in the markets. But we believe that hypergrowth stocks are very close to one. And now may be the time to start buying the dip.

Because weaker consumer confidence leads to less spending. Less spending leads to lower inflation on the demand side. This could very well be what the Federal Reserve is hoping for. That is, as the specter of higher rates takes down all assets (crypto, equities, housing), consumer spending is curtailed. And demand hits a slowdown. And this is coinciding with the normalization of global supply chains. Supply spikes, and demand takes a dive.

That’s bullish for a slowdown in inflation.

However, consumer credit numbers are hitting new highs, which could signal they’re still spending by maxing out their credit cards. After all, folks still need food, housing and transportation. So, spending can only be curbed by so much.

So proceed with caution. If you buy the dip, make sure to only invest what you can afford to lose. Take a nibble here and there by cost-averaging down into your positions. If growth stocks do have further to fall, the drops will be swift. By cost-averaging, you can limit your downside while allowing for further upside when the market rallies again. Don’t buy the dip all at once.

Growth Stocks Win Once the Crash Passes

At the top of this note, we wrote that we’re very bullish on a certain group of stocks at the current moment. That group is hypergrowth tech stocks.

I know. That may sound counterintuitive. But follow me here…

In our flagship investment research product Early Stage Investor, we invest in stocks for the long-haul. We’ve identified a particular group of stocks that have been unnecessarily battered despite sporting rising earnings and revenues. And these stocks have a very good chance of snapping back to all-time highs.

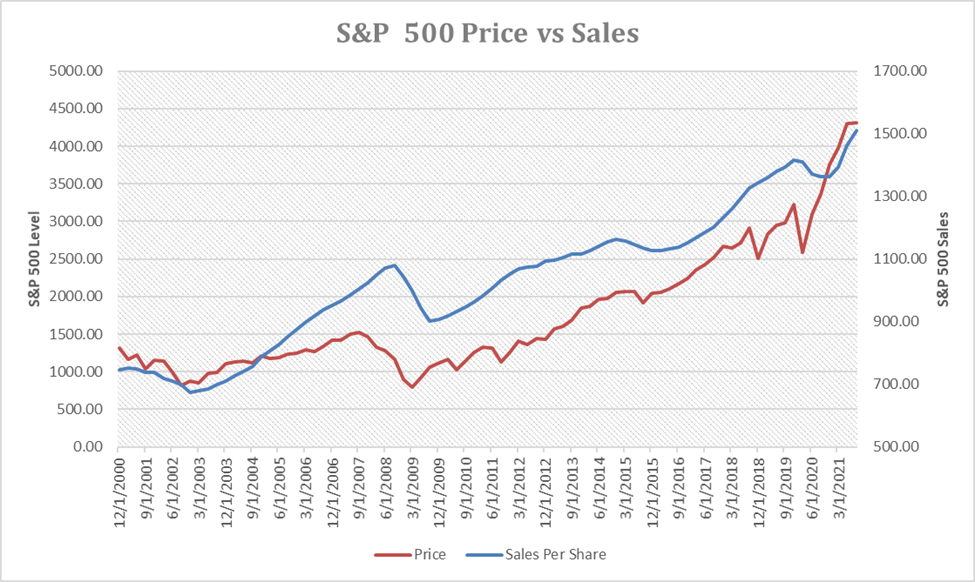

See the chart below, which illustrates the strong positive correlation between S&P 500 price and sales. Numerically, this is a positive correlation of 0.88, or nearly perfectly correlated. You don’t get much more closely correlated than that in the real world.

Regardless of a recession, solid growth companies will continue to grow their revenues and earnings at a very healthy rate over the next several years.

In other words, their “blue lines” from the above chart will continue to move up and to the right. Eventually, their “red lines” — or their stock prices — will follow suit.

That’s why we’re very bullish on growth stocks today.

Their blue lines (revenues) continue to go higher and higher, while their red lines (stock prices) are dropping sharply. This is an irrational divergence that emerges about once a decade during times of economic crisis. And it always resolves in a rapid convergence, wherein the stock prices rally to catch the revenues.

Bear Market Opportunity in Growth Stocks

Despite the present market climate, now is not the time to freak out.

Remember: Crises create opportunities. In stocks, this has been the case forever. This time is not different.

And, in the current crisis, the opportunity is particularly large in growth stocks. We fully believe that once this bear market ends — and it will — certain growth stocks will rattle off 100%, 200%, and even 300%-plus gains.

The investment implication? It’s time to hunker down in the right growth stocks.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.